Download results in pdf

Download results in pdfCompound interest: How it works and how to apply it

By not taking advantage of compounding, you could be missing out on significant savings. Compounding can help you achieve your financial goals faster — whether it's buying a new car, upgrading to a larger home or taking more holidays.

Albert Einstein famously called compound interest the 'eighth wonder of the world', and with good reason. The Nobel Prize-winning physicist understood the power of numbers. In personal finance, compounding can have a huge impact on building wealth.

1. What is compound interest? A beginner's guide

How simple interest works

We've all learnt about percentages at school — they represent a proportion of something. For example, suppose John shares an apple with Jane, who bites off half of it. Now John only has 50% of the apple left. In mathematics, 50% is simply half or ½ of the whole.

Percentages also play an important role in statistics. They help us to understand growth or change in relation to an initial value. Consider a factory that produced 100,000 shoehorns in 2021. Due to increased demand for its stylish and functional designs, it increases production to 120,000 units in 2022 — a 20% increase in output.

But the most common use of interest relates to money, which is where our focus lies.

Interests are all about money, and this is what interests us the most!

For example, if you deposit money in a bank, you may earn 10% interest. If you deposit $1000, after a year you'll have $1100. That's simple interest at work.

How compound interest works

Compound interest, on the other hand, comes into play when you reinvest the earnings you receive. Allowing your total balance to grow even faster as you begin earning interest on both the original amount and the added interest.

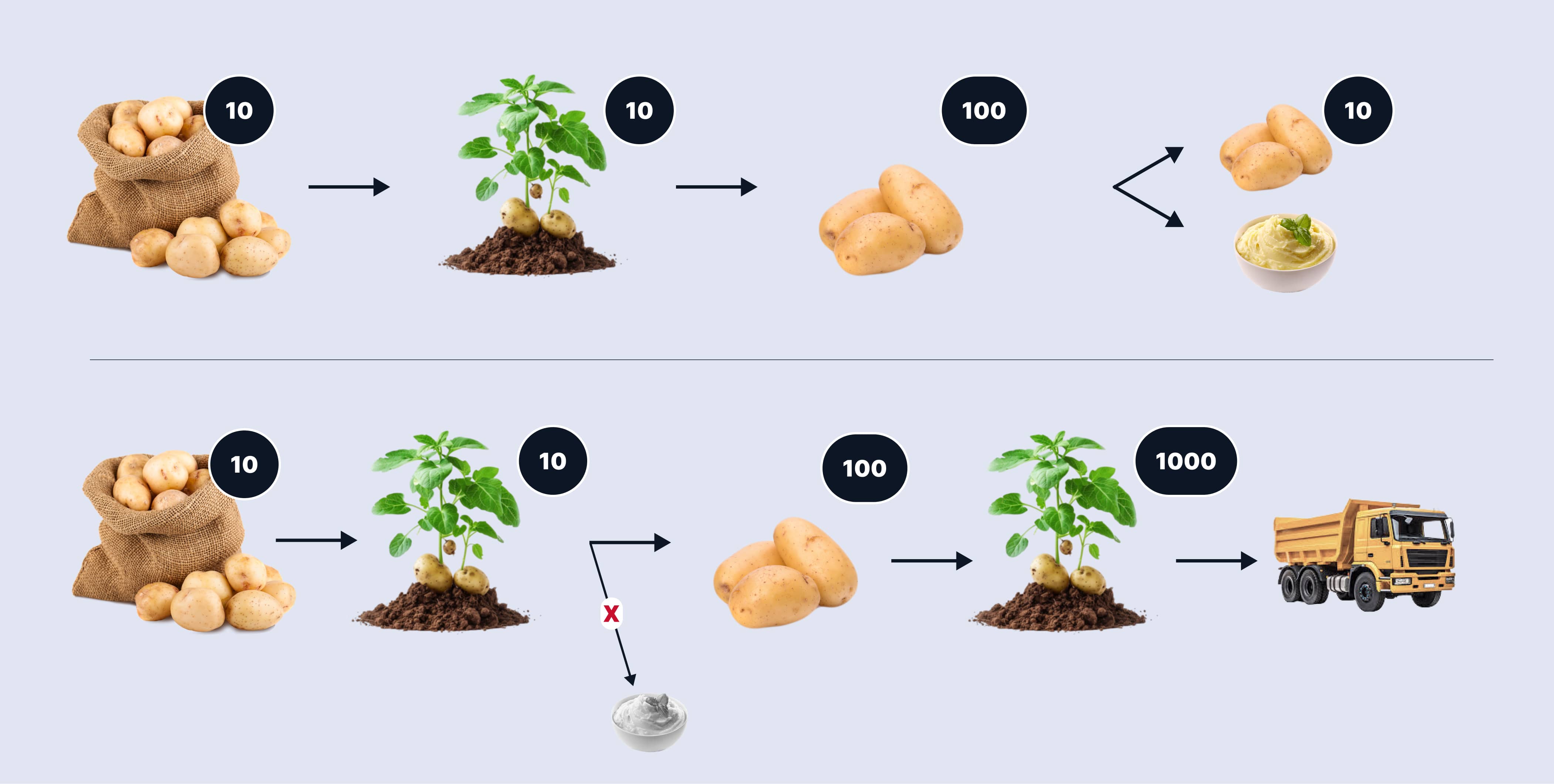

The easiest way to explain this is with a farming analogy — let's look at potatoes.

An experienced gardener bought 10 top quality potato tubers. In fall, he harvested 3 buckets of potatoes, or 100 tubers. He could have eaten almost all of them, leaving 10 tubers to plant next year.

But this gardener is smart. Instead of using up his entire crop, he planted all 100 tubers the following spring. By fall, his yield has skyrocketed to 30 buckets, or 1000 tubers. Now he has plenty to eat, replant, and even sell to the neighbors, earning back what he invested two years ago.

The same thing happens with money with the potatoes.

Imagine you have $5,000 in your bank account earning 10% interest annually. Each year you receive $500, which is 10% of your original investment.You could withdraw that $500 each year and continue to invest the original $5,000 at 10% per year.

If you use this method for five years, your total earnings will be $2,500 ($500 × 5 years = $2,500).

But there's another way — you can invest your earnings back into your initial deposit. After the first year, you'll earn 10% on $5,000, or $500. But in the second year, you'll already earn 10% on $5,500, which is $550.

That extra $50 is the result of compound interest. You didn't add anything or do anything extra, yet you made more money.

2. How compound interest works

Let's take a closer look at this process with a more specific example.

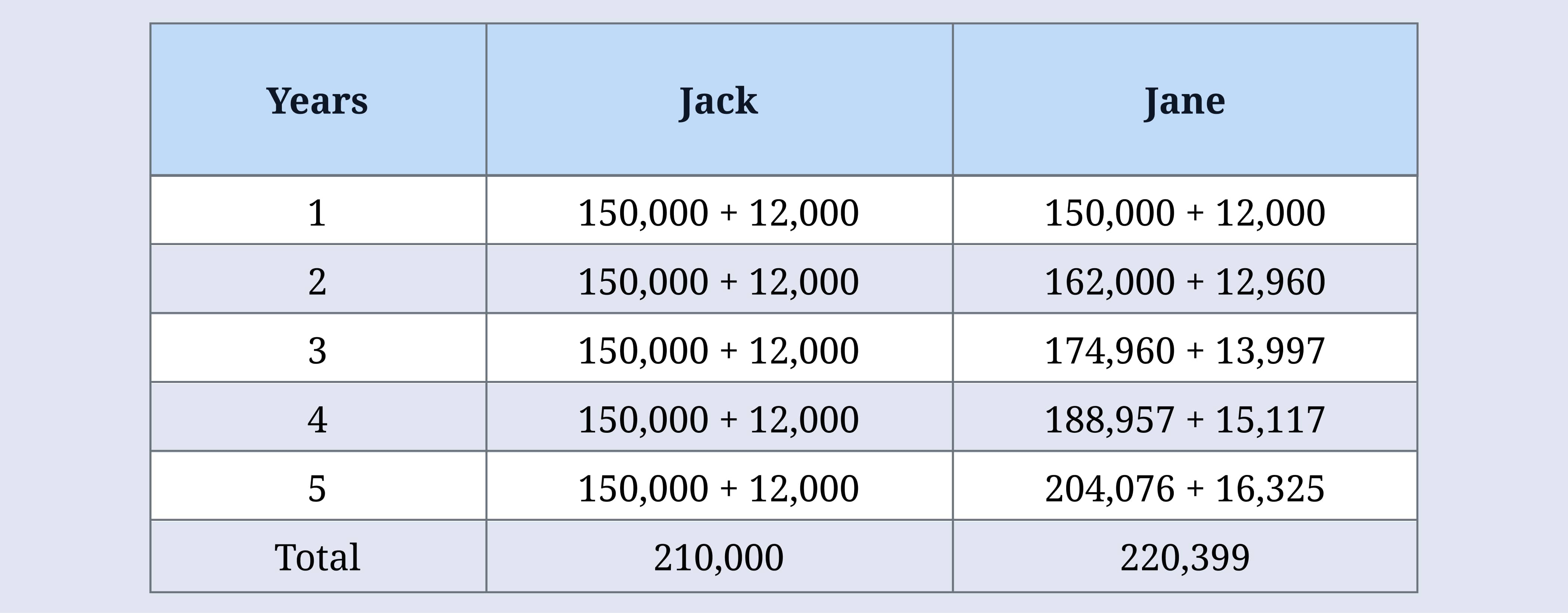

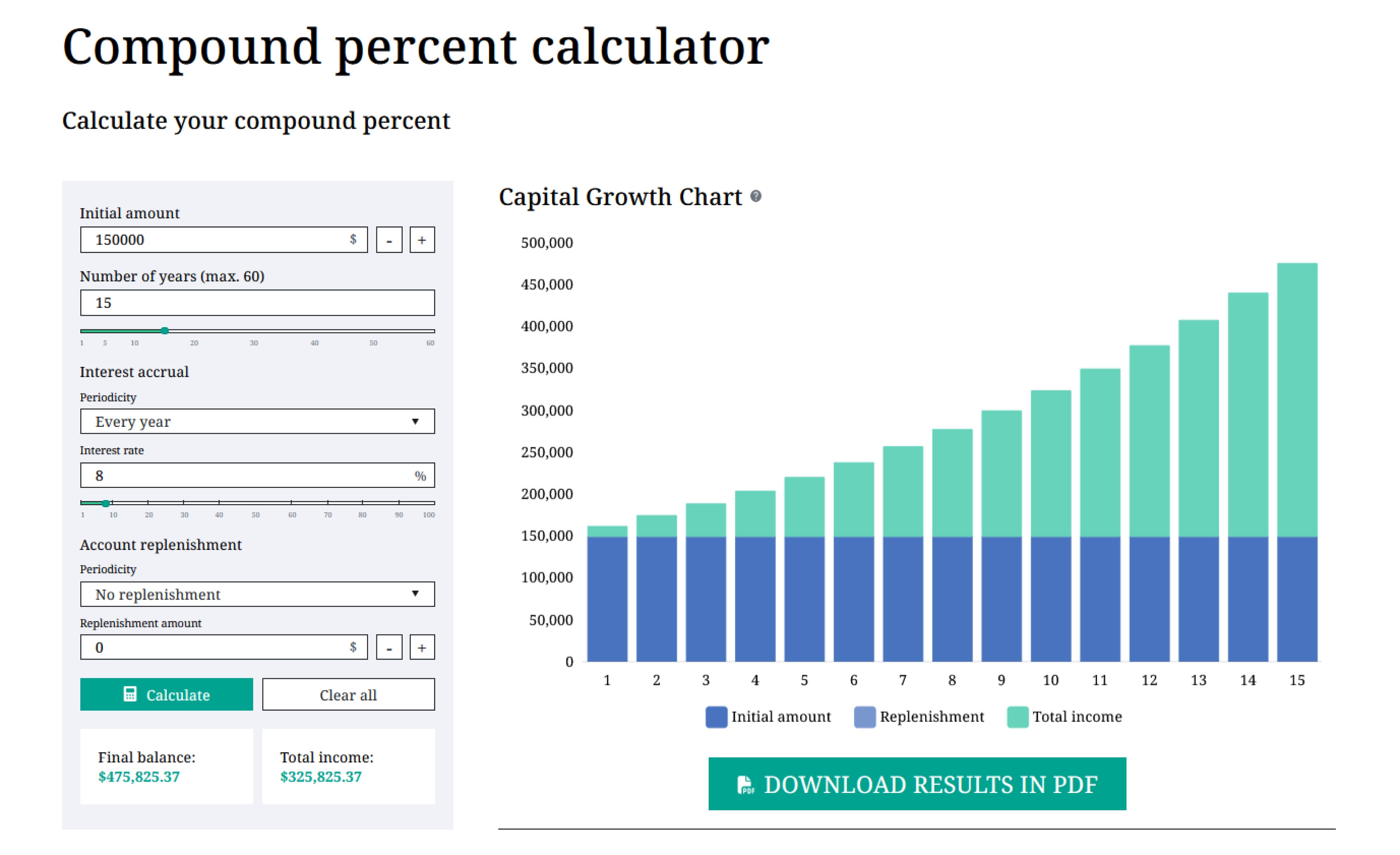

Imagine two investors, again named Jane and Jack. They both start with the same initial capital of $150,000. They invest in 5-year bonds that pay 8% per year. However, Jack uses the simple interest strategy — he withdraws and spends the income each year. Jane, on the other hand, uses the compounding strategy — she reinvests her earnings in new bonds each year.

This strategy is called reinvestment.

Reinvestment is the practice of using profits from previous investments to make new investments, helping to grow your income further.

The formula for calculating compound interest is shown below:

- S is the final amount including compound interest

- P is the initial investment

- i is the simple interest rate (annual interest rate)

- m is the number of times the interest is compounded per year

- n is the investment term in years

Now let's calculate the amount Jane will receive after investing in bonds for five years:

After rounding, Jane will receive $220,399. During the same period, Jack, using the simple interest strategy, will receive $150,000 + ($12,000 × 5) = $210,000.

The table below shows how the income from Jack's and Jane's investments has grown over the five-year period.

3. Capital growth chart

When calculating compound interest, a snowball effect is observed.

The main advantage of compounding is that your profit increases every year. The longer you invest, the greater the final result. Let's look at how Jack and Jane's investments performed over a longer period of time — 10 and 15 years. We'll also include their five-year results for comparison.

Jack

Jack receives $60,000 of income every 5 years, or $12,000 per year.

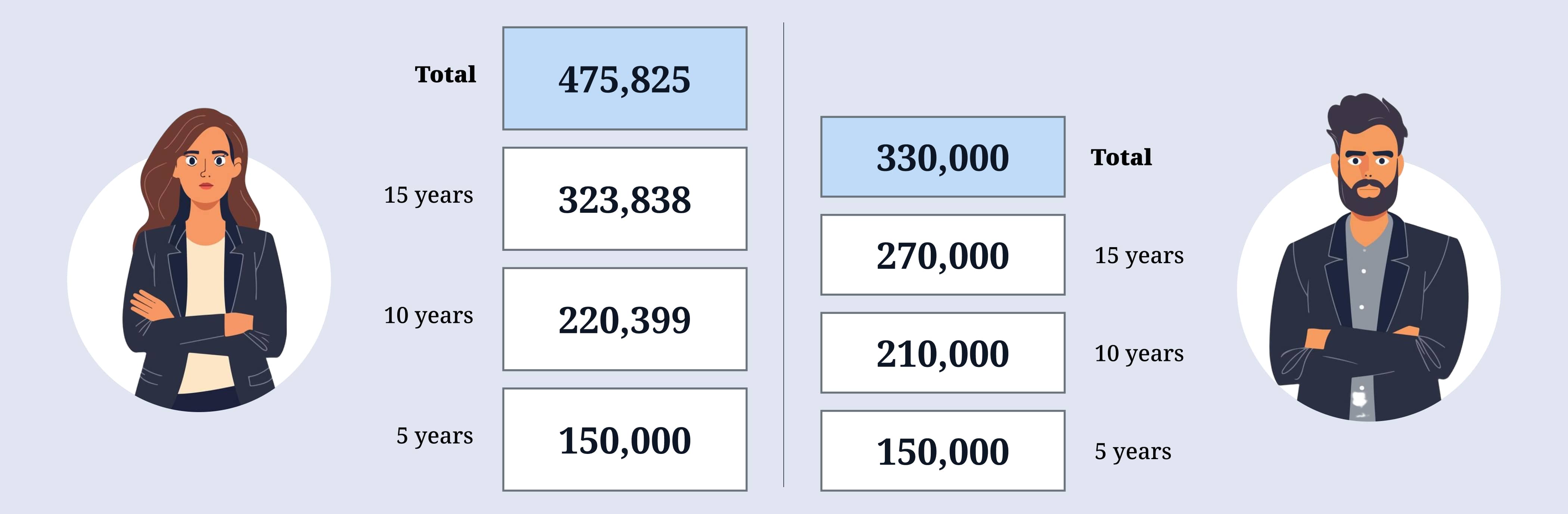

After 10 years, Jack's total will be $270,000, consisting of his initial $150,000 and $120,000 in interest that he has spent.

After 15 years, his total investment growth will be:

$150,000 + (15 x $12,000) = $330,000

At the end of 15 years, Jack will have saved his initial deposit of $150,000 and earned $170,000 in interest - slightly more than his initial deposit.

Jane

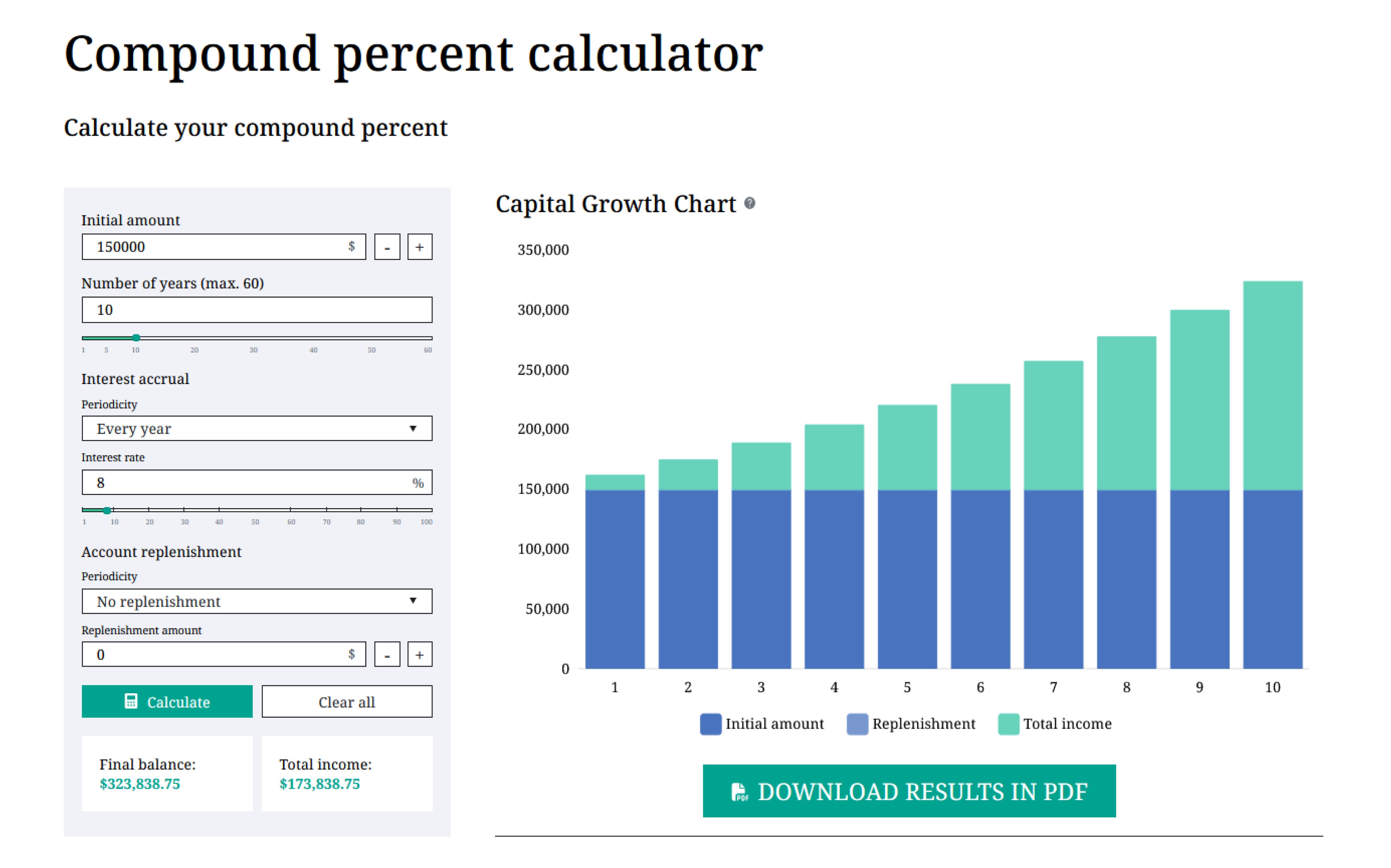

To calculate Jane's income, we'll use the convenient online calculator available here. This tool allows you to automatically calculate different income scenarios, eliminating the need for manual calculations and reducing the risk of error.

4. Calculations

After 10 years of reinvesting her earnings, Jane's account will grow to nearly $324,000. She will have earned $173,838 in interest alone, which is almost 1.5 times more than Jack's interest over the same period ($120,000 out of a total of $270,000).

Jane's initial capital will have doubled in 10 years, while it took Jack nearly 15 years to achieve the same result.

Over a 15-year period, the difference between their results will be even more significant.

With an initial investment of $150,000, Jane will earn $325,825 in interest over 15 years — more than double her initial investment. Her final account balance will exceed $475,000.

Let's compare the returns on Jack's and Jane's investments over this period.

Jane tripled her investment over 15 years, while Jack only doubled his. Even though they both started with $150,000 and used the same financial instrument — bonds.

There's no magic involved, just simple math.

5. Where can compound interest be used?

Bank

You can open a savings account at a bank.

Some deposits include automatic interest capitalization in their terms. This means that the bank adds the accrued interest to your deposit and continues to earn interest on that amount.

If the interest is sent to a separate account with a low interest rate, be sure to withdraw it regularly and reinvest it at a more favorable rate.

Stock market

You can also benefit from compounding by investing in financial instruments such as dividend stocks, ETFs and bonds. The income you receive from dividends and bond coupons can be reinvested to buy more financial instruments, such as additional bonds or diversified investments.

By reinvesting, you are continuously investing your gains over the life of the investment.

Unlike automatic bank capitalization, stock market investments require active management. Bonds won't buy themselves — you need to take action.

6. Possible disadvantages of compound interest

Over a 10-15 year period, the economy may fluctuate. Interest rates may fall, requiring you to adjust your income projections. Still, the magic of compounding will outshine the returns from passive investing and spending additional income.

Jane's returns will consistently surpass Jack's.

Inflation is another potential risk, as it can erode your earnings and reduce the real value of your money over time. It's important to factor this into your savings growth plan.

7. An additional factor affecting compound interest

Remember that income from bank deposits and profits from stock market investments are subject to taxes, which will affect the final amount of your savings.

8. How to use the compound interest calculator

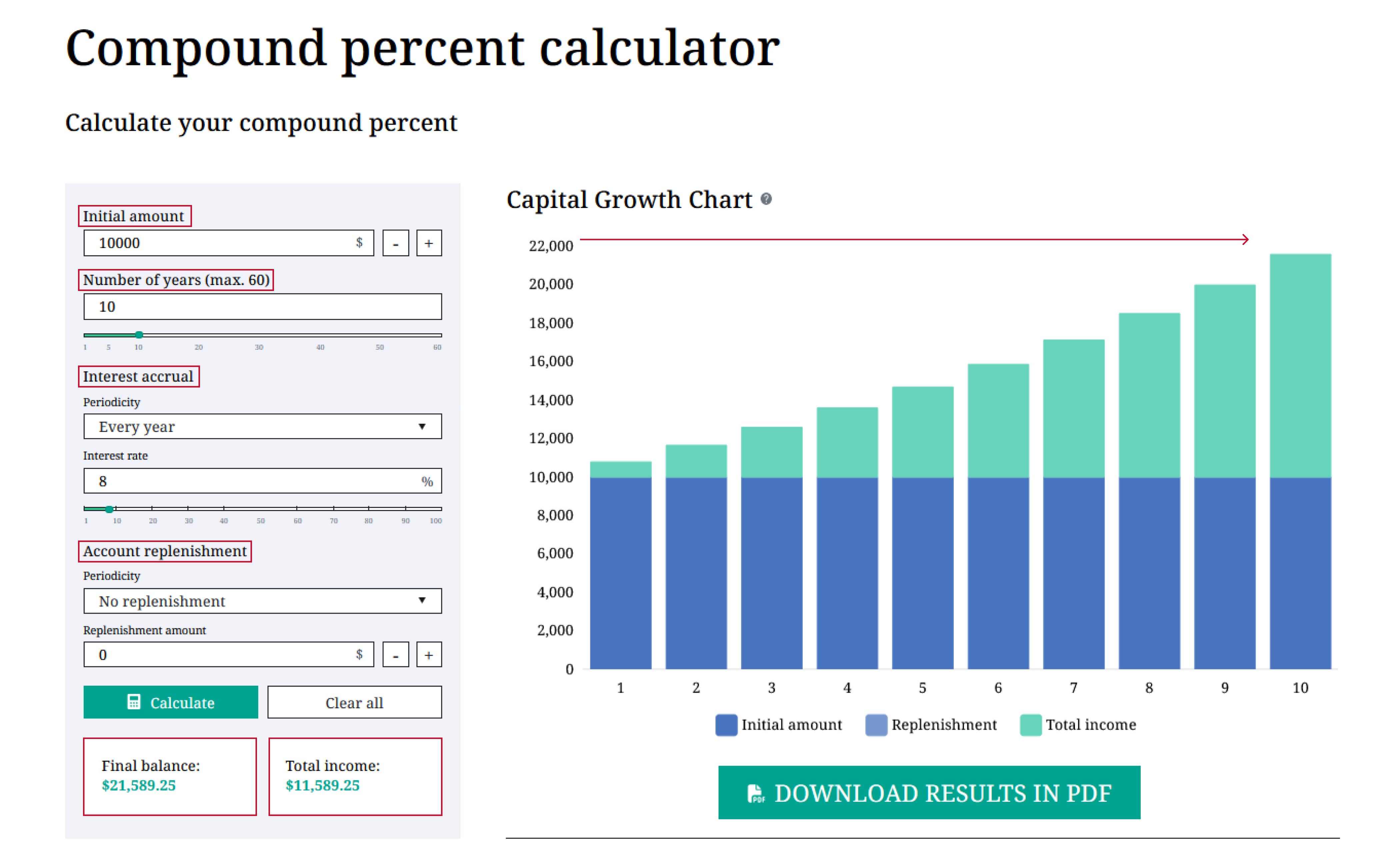

The compounding calculator allows you to enter various investment parameters:

- Initial amount, which is the starting capital you want to invest

- Number of years, where the maximum number is 60

- Frequency of interest accrual - yearly, quarterly, monthly

- Interest rate offered by your bank

In addition, you can change the account replenishment parameters. There can also be no replenishments set.

Click on the CALCULATE button to get your final balance and total income, visualized in the form of a chart and a table.

You can take a look at our FAQ section below if you have more questions. We wish you good luck in the markets!

Frequently Asked Questions

Is it possible to make calculations for deposits without replenishment?

The calculator allows you to calculate the profitability of both replenished and non-replenished deposits.

What interest accrual frequency can be entered into the calculator?

Calculation options include monthly, quarterly and annually interest accrual.

Is it possible to set the rate to 0%?

No, in this case our calculator will not allow further calculations.

Can the initial amount be equal to 0?

No, it should be equal or greater than $1.

Can the amount of replenishments be equal to 0?

Yes. Navigate to the "Frequency of replenishment" field, and press the "No replenishment" button.

What is the maximum number of years that can be entered into the calculator?

The available range for calculations is from 1 to 60 years.

What is the maximum amount that can be entered into the calculator?

For the simplicity of calculations it's limited to $100 million, which should cover most, if not all possible situations.

Is it possible to receive calculations in printed form, rather than on a computer screen?

Yes, the calculator has functionality of creating a PDF report.

If I need to calculate something else, are there other calculators on the website?

Yes, the links are in the header of our website - you will find calculators and other tools there. For example, there is a Futures Calculator and Trade Return Calculator.

Curious to learn more?

Get your hands on Max Schulz’s book by downloading it today! Free of charge.